A Year In Review – Looking Behind The Headlines To Get Ahead In 2024

Property investment has – and always will be – a long-term game. Many investors fret when the market experiences its typical ebbs and flows, and may feel pressured to offload parts of their portfolio when news headlines suggest that disaster is on the horizon. However, it is important to remember that news outlets often dramatize the reality of the situation in order to gain clicks and views, and many of their fear mongering predictions have simply not held up.

In this piece, we’ll looking at the year in review, guiding you through four headlines from the past year and reviewing whether they actually came to fruition.

UK house price crash: Homeowners warned values could plunge by up to 40% in huge blow

This headline issued by the Express caused quite the panic among homeowners and investors, suggesting that 2023 could see a housing crash on a drastic scale. The Bank Of England base rate rises were said to be to blame for this upcoming crash, with the Express believing that this would severely stifle buyer’s desire to purchase property.

What the Express didn’t quite take into account was the huge imbalance between supply and demand which continues to fuel the property market. Competition for property is exceptionally fierce as there are plenty of searching buyers, and not enough properties. In fact, Britain has a backlog of 4.3 million homes that are missing from the national housing market – a deficit that could take half a century to correct, even if the government’s current target of building 300,000 units per year is reached. This meant that despite the frequent base rate rises, demand was still high, and prices did not crash by 40%.

This isn’t to say that the base rate rises have had no impact. They did cause an average dip in property values by 5.3% between January and August 2023, but this was far less impactful than the anticipated 40% slump. In fact, several areas across the UK have actually experienced growth or a much lower reduction in prices. Furthermore, it is important to note that the government have put measures in place such as the cuts to Stamp Duty Land Tax to help avoid a crash by keeping demand high.

As we look to away from the year in review and towards the future of the market, it is likely that the number of property transactions will slip more than prices. Many will choose to stay in the rental market until prices settle, which is good news for investors as the amount of competition for high quality investment units will be less fierce and rental demand will continue to grow.

UK house prices forecast to fall for the next two years

https://www.bbc.co.uk/news/business-63676119

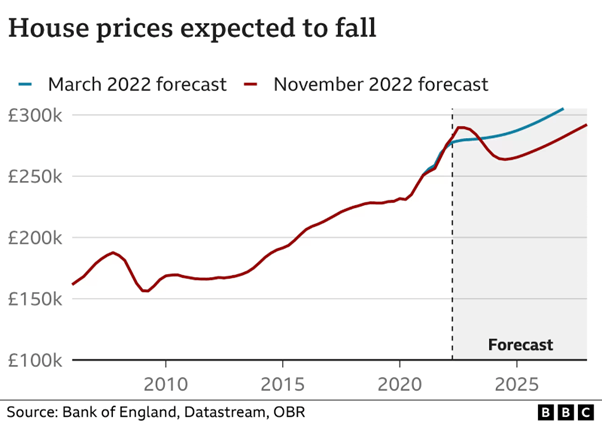

A BBC news report from Winter 2022 suggested that UK house prices would fall significantly until 2024. Based on research conducted by the Office of Budget Responsibility, the BBC reported that it would take even longer for the property market to rebound from its slump, as suggested by the diagram below.

The reality of this price slump is far less dramatic than anticipated. According to Halifax, there was a 2.6% price reduction in 12 months to June 23, demonstrating that the market has been relatively resilient in the face of the fastest interest rate hike in more than 35 years.

However, it is important to note that both forecasts shown in the graph suggest an upwards trajectory for property prices, with this slump only being a temporary ‘blip’ in the market. These peaks and troughs are normal and should not disrupt investors’ long-term growth strategy. Joseph Mews’ Marketing Manager Johnny Conran summed this up by stating that “property investment is a long term strategy – we’re not talking about an immediate return in a year or two. If you’re taking out a mortgage, it forms part of a 10 to 20 year investment plan”.

In this market, flipping property in the short term is often not viable, with high Stamp Duty and mortgage costs meaning that immediate ROI is unlikely, so buyers are encouraged to hold their assets for the long term. This will allow them to benefit from the fantastic anticipated growth that could see the average property price soar past £300,000 by 2027.

So what does this mean for investors? Investors should be cautious when offloading assets as a result of dramatic news reports such as these, and should be aware that market corrections like these are completely normal. As the above graph demonstrates, even the 2008 housing crash corrected itself, showing that market corrections like the one we are currently experiencing have happened before and have not hampered long-term price growth. Pre-2007 peak property prices have now increased by 51% across the UK, and the average price of property has doubled since 2004 according to the House Price Index, with investors that have held on to their assets seeing a huge return on their investments.

Additionally, Savills predict that by 2026 there will be a huge 7% increase in house prices, meaning that now may be the best time to secure new investment properties at a lower price. So, it is strongly advised that investors hold out to reap the rewards of long-term market growth.

“Property prices keep going up. There will be a blip, and then they will continue to go up again. There will probably be a couple of corrections over the next 10, 15 years, but you will always end up with a more valuable property at the end compared to what you buy now” – Liam Smith, Head of Residential Investment at Knight Frank

Public confidence in Bank of England’s inflation strategy hits record low

https://www.ft.com/content/f70dc1b8-97ed-4522-9da8-718a7c5127ae

When looking at the year in review, the Bank of England’s decision to increase its base rate on fourteen consecutive occasions has had a very tangible impact on the property market. The Bank are attempting to bring down inflation by hiking interest rates, which has put stress on the property market by hampering affordability. As a result, public confidence in the bank has hit a record low. But is this lack of confidence in the Bank of England’s choices, and the subsequent impact this has had on the property market, really warranted?

Inflation has already started to fall over the last few months, and is expected to reach 5% by the end of 2023 before hitting just 2% by 2025. This will mitigate the cost of living crisis and make price hikes much more manageable to deal with which, in turn, will make property more affordable.

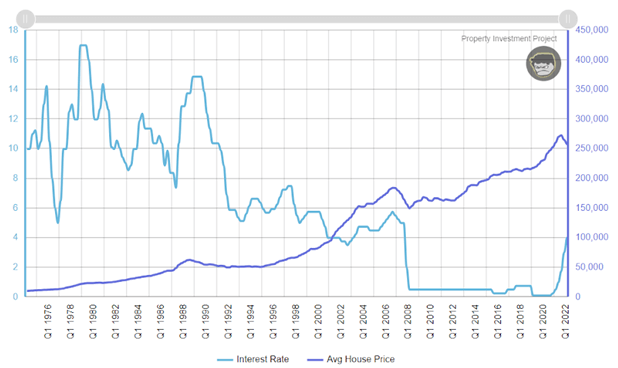

It is important to note that the past fifteen years have been unusual when it comes to the base rate. Prior to 2008 the base rate rarely fell below 5% and currently sits at 5.25%, and before 2008 the lowest the BOE interest rate had ever been since 1975 was 3% for a very short period. In the grand scheme of things, the current interest rate isn’t actually that high. Furthermore, as the graph below demonstrates, property prices have continued to rise and strengthen despite changes to the base rate over time. The peaks and troughs of the base rate throughout the 1970s and 80s had little to no impact on house prices, showing that an increase to the base rate does not equal Armageddon for property prices. Many more factors, such as supply and demand, contribute to the strength and affordability of the market.

Increased mortgage costs as a result of the base rate increases can be offset by higher rental prices in desirable areas. For example, Savills note that Birmingham rental prices are set to increase by 19.3% between 2023 and 2027. The rising cost of renting has again hit its highest level since comparable records began in 2016, with strong demand from tenants. Such strong tenant demand means that rising rental prices will be accepted among the exceptionally competitive pool of searching tenants.

Get Ahead Of The Headlines With Joseph Mews

If our year in review shows anything, it’s that news headlines aren’t always accurate, and certainly don’t take into account the resilience of the UK property market. In fact, property remains one of the most promising assets to invest in, and has historically been able to weather any storm.

If you are searching for your next investment property to add to your portfolio, or want to take your first steps towards investing in this resilient asset class, contact Joseph Mews or explore our selection of investment-ready developments here.